| |

|

|

|

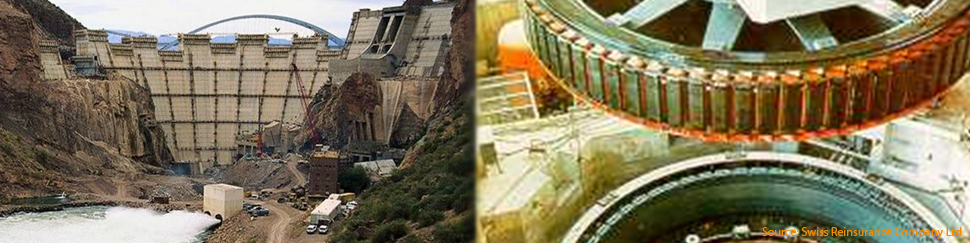

Erection All Risks Insurance

Erection All Risks Insurance is designed to cover risk arising from installation and erection of engineering project such as power plants, refrigeration plants, electrical generator stations, overhead gantry cranes, machinery, equipment, and so on. It provides financial security for all parties involved in an installation and erection project including testing and commissioning risk.

Scope of Cover

-

Testing and Commissioning Risk cover loss, destruction and/ or damage to the property insured occuring during testing and commissioning work carried out by the contractor or sub contractor involved:

- Testing of various kinds

- Commissioning, i.e. initial operation

- Maintenance

- Operation of the completed works

-

During the construction period the standard policy covers the contract works against unforeseen, physical and accidental damage from any cause not specifically excluded in the policy including:

- Fire, lightning and explosion

- Faulty manipulation or handling

- Water damages, flood, storm and typhoon

- Collapse, landslide, earthquake, volcanic eruption

- Burglary, theft, malicious damage

- Consequence of defective material and/ or workmanship

-

Third Party Liability Section:

Under the Third Party Liability (TPL) Section, cover up to a reasonable limit of indemnity, generally not in excess of USD 2 millions, is available for damage or injury or loss caused to third parties by the works activities on or in the immediate vicinity of the site.

-

Insurance Period

The insurance period is started immediately after uploading on the site and includes

- Storage on the site

- Construction and erection

- Cold test

- Hot test

And ended when the project has been handed over or put into commercial operation.

-

Insured Parties

A main feature is to protect all those who have an immediate economic interest in the project ("insurable interest"):

- The principal

- The contractor and all subcontractors

The advantage of insuring all the interested parties under the same policy is twofold:

- No time-consuming disputes in apportioning blame; i.e. repairs can commence quickly after notifying CAMINCO.

- No gaps in insurance cover which can happen in the case of individual policies.

- Maintenance

Contractor's All Risk Insurance (CAR) policy may be extended to the maintenance period by specific endorsements:

- Visits Maintenance: The constractor is insured against any loss or damage he may cause during the maintenance period to the property insured under the Material Damage section of the policy whilst performing any constractual maintenance obligation at the site.

- Extended Maintenance: Cover is granted as under "Visits Maintenance", however, it is extended to loss or damage which may arise from any act or omission of the contractor at the site during the contract works period.

Underwriting Information

- The insured, the principle and other parties that have interests from the project.

- Total Sum insured breakdown: basic contract details and values

- Temrs and Condition (Inquiry slip), Site or Plant layout plan and sections, project schedule.

- Soil (Underground Geological Condition) Investigation, foundation design report and major equipment spec.

Why you need Erection All Risks Insurance (EAR)

- Erection All Risks Insurance policy is needed when constractor undertakes any type of constraction work.

- The constractor has responsibilities and obligations towards the principal and any third-parties who may be involved and affeced. As a result of this, the constractor shall be protected these obligations by this insurance policy.

Claim Procedure

- In case of the event may give rise to a claim, the contractor will

- Notify CAMINCO directly or via agent/ broker immedately

- Submit completed claim form or the loss adjuster's report providing most the information needed to ascertain whether or not the loss is covered.

-

Where the loss is complicated, CAMINCO will appoint a loss adjuster to prepare a report, and the insured will provide the following information to the loss adjuster:

- The value of property prior to or after loss

- The extent of loss or damage

- The cause of loss or damage

- The likely cost to repair

- Any uninsured element (apart from the deductible)

- The effect of extensive delays to the work

|

|

|